Argentina: World Cup Is Over; Bigger Match to Come in Presidential Election

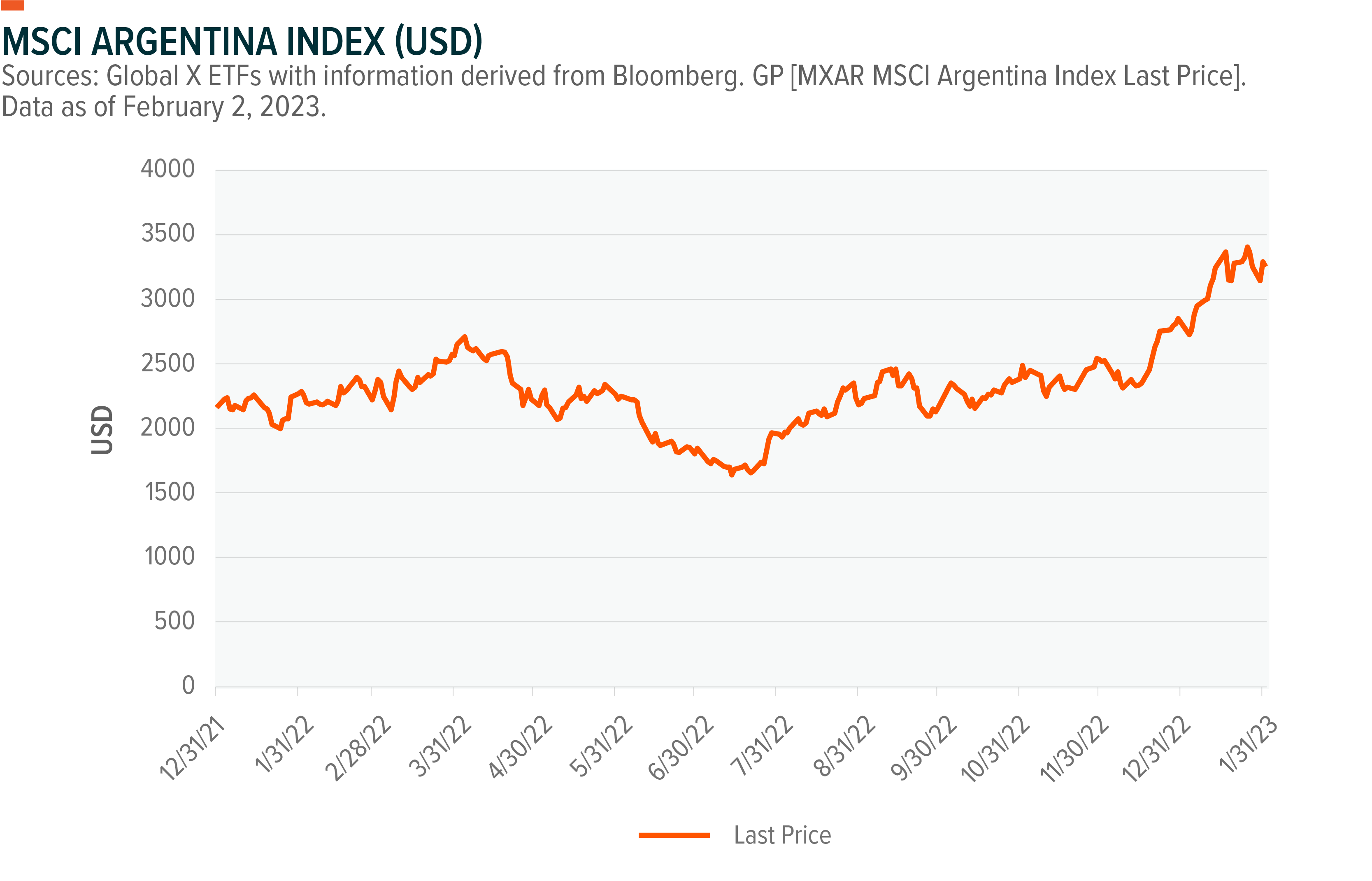

A World Cup championship isn’t the only thing Argentina has had to smile about recently. After tumbling over 50% in 2018 and 20% in 2019, Argentine equities (as measured by the broad MSCI Argentina Index) have quietly stabilized and returned 12.70%, 20.95%, and a whopping 35.91% respectively over the past three years (in USD terms). 1 Argentina’s market has begun this year on the right foot as well, with the index rising 19.35% YTD as of January 26, 2023. 2 Key drivers of the recent rally include proximity to this year’s presidential election, US dollar weakness, and China’s reopening.

Despite the strong run, fundamentals still appear relatively attractive, as the market was trading at 3.71x earnings and 0.61x book value (vs. 18.29x and 3.82x for the S&P 500 Index and 10.65x and 1.51x for the broader MSCI Emerging Markets Index). 3 Though valuation multiples look inexpensive, fundamentals are difficult to analyze amidst hyper-inflation. Politics and macroeconomics look poised to drive near-term performance. With growing pressure on solvency accompanied with a potential change in governance, 2023 will be an important year in the quest to revitalize Argentina’s economy.

Stabilizing the macroeconomic picture will be an important step towards tapping into Argentina’s potential.

Election Remains Focal Point

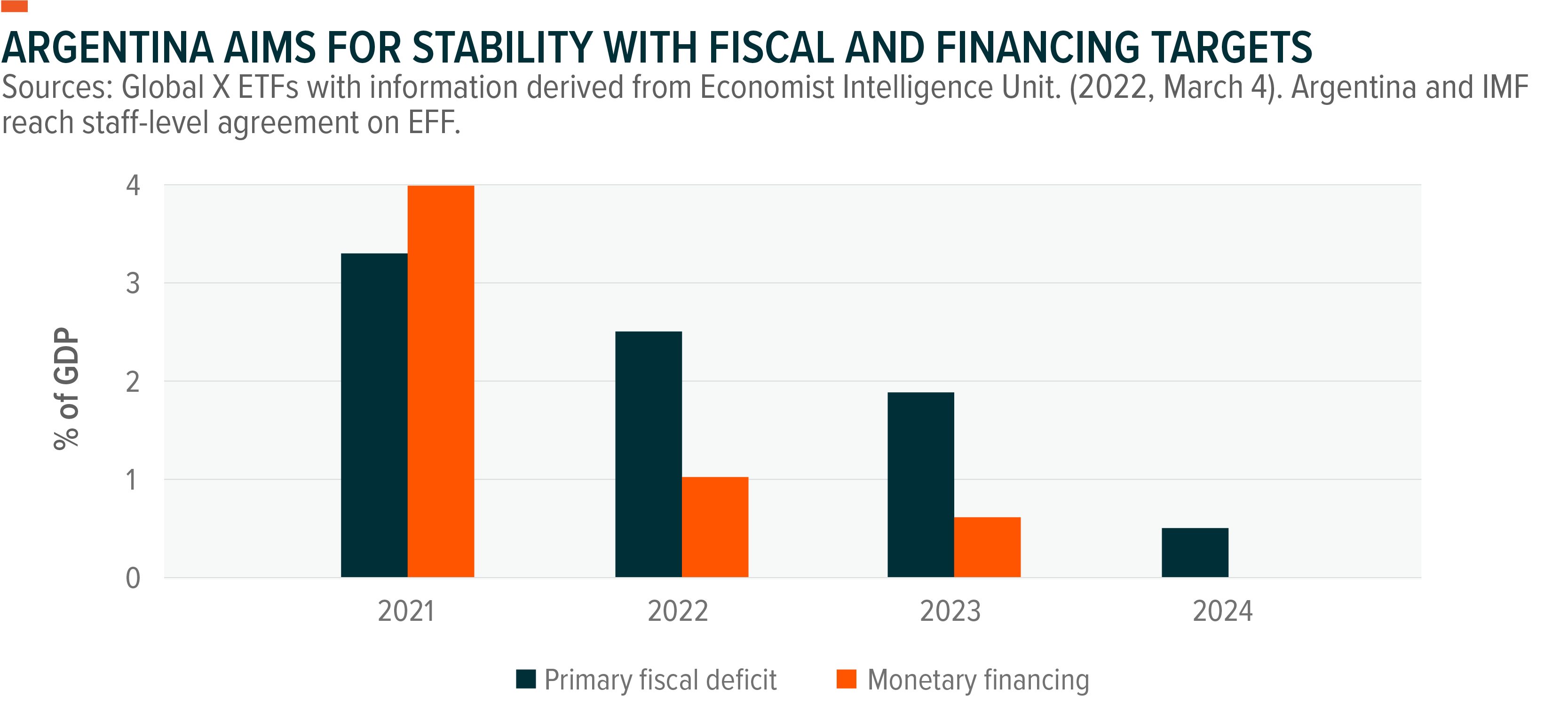

Curbing excess spending and taming inflation have been paramount goals for Argentina in recent years. Argentina’s relationship with the International Monetary Fund (IMF) is also closely observed by investors for that reason. In 2018, the IMF and Argentina agreed on a USD $50bn line of credit, which was extended in March of 2022. In this program, the IMF provides monetary support in exchange for commitments for the country to focus on inclusive growth, contain inflation, manage its balance sheet, and address gaps in infrastructure.

In 2022, uncertainty increased when three Ministers of Economy (MOE) took office within the span of a month between July and August. Since then, the position of MOE is in a more stable and predictable state, with Sergio Massa running a campaign of relative fiscal responsibility. There is still a debate over the expansion of the Ministry of Economy, which has resulted in Massa being dubbed the “Superminister.” Markets are watching closely to see how Massa navigates the balancing act between the ruling coalition and the IMF as the presidential election approaches. Massa entered his position with praise from the IMF, and maintaining that working relationship will be crucial to keep Argentina moving in the right direction.

Although it is still too early to predict the outcome, the presidential election could lead to a change in government and fiscal reforms that would likely attract attention from the investment community. New political leadership would open the door for additional economic reforms that could include new policies on spending, currency controls, and other orthodox economic measures. Such actions would hold potential to improve the country’s credit profile, attract foreign direct investment, support the peso, tame inflation, and eventually leave room for the central bank to normalize interest rates. It may be the case that the recent rally was driven by increasing expectations for change and reform, especially after the October election.

Argentina’s Potential Spans Diverse Sectors

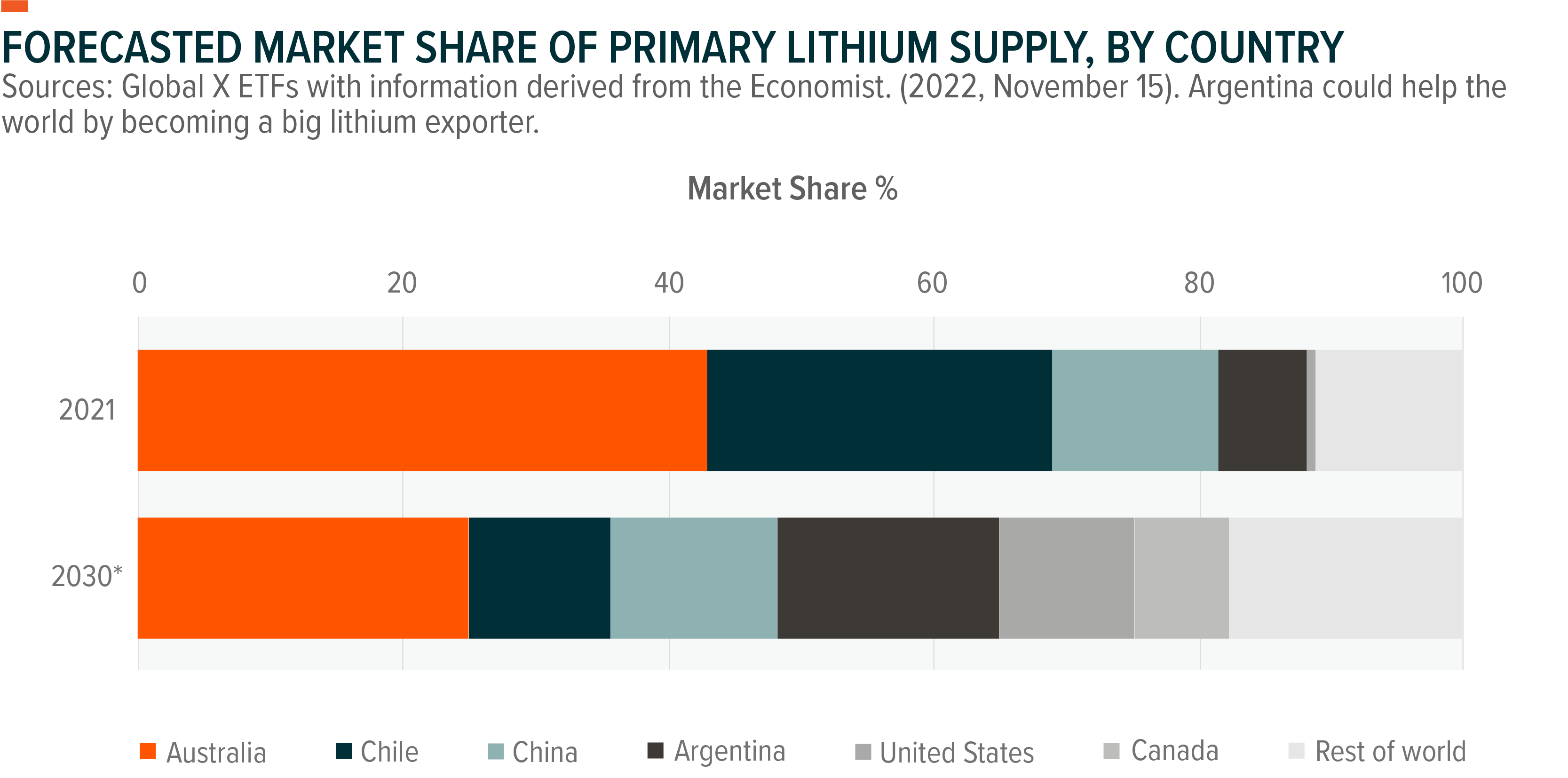

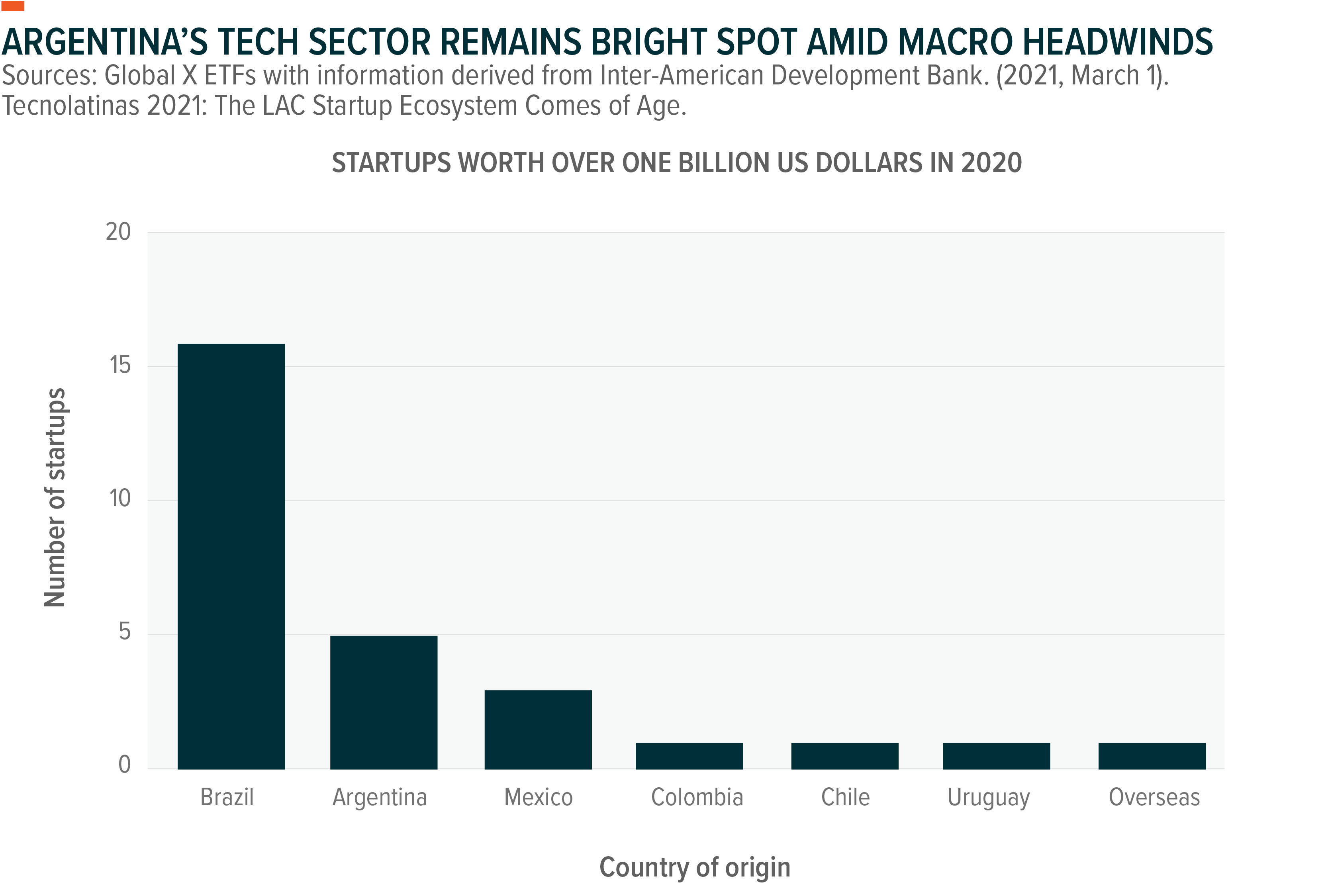

While challenges and uncertainty exist along the way, if Argentina can succeed in stabilizing the macroeconomic picture, that would go a long way in unleashing Argentina’s potential. The government estimates that $300bn of wealth is being held abroad by Argentines in the US, and the return of some of that wealth to the country will likely occur if investor confidence improves. 4 Furthermore, Argentina is rich with natural resources that it has not fully tapped into yet. As part of the “Lithium Triangle” in the Andean region, which is home to two-thirds of global lithium supply, a more stable Argentina would become even more important in the global lithium supply chain.5 Argentina’s leadership in the tech and e-commerce spaces also stands out within Latin America, with the e-commerce giant MercadoLibre being the largest online marketplace in the region.

Unpacking the MSCI All Argentina 25/50 Index

Energy companies YPF and Pampa Energia (PAM) together make up roughly 12% of the MSCI All Argentina 25/50 Index.6 As both names have positive correlations with crude oil, higher energy prices could also benefit Argentina’s momentum. While YPF has a correlation of 0.515 with crude oil, PAM’s correlation is at 0.405, as of January 18, 2023.7

The Global X MSCI Argentina ETF (ARGT), which seeks to track the MSCI All Argentina 25/50 Index, carries a combined exposure of approximately 13% to those names, but also holds a 20% position in MercadoLibre, which could be a key beneficiary of the end of monetary hiking cycles in the US, Brazil, and Mexico.8 In addition, Lojas Americanas, one of MercadoLibre’s largest competitors in Brazil, just filed for bankruptcy, which should provide runway for more market share gains.

Related ETFs

ARGT – Global X MSCI Argentina ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.