Exchange Traded Options Market Making, Explained

The following is Part 1 in a 3-part blog series on the market making landscape for exchange traded options. This part elaborates on the role of liquidity providers when it comes to making a market in listed options. Part 2 will discuss additional market maker option risk hedging needs while Part 3 will discuss potential option market impacts on market volatility and considerations when analyzing the growth in ETF usage of such contract types.

Investors have two ways to access options markets: exchange-listed options or over-the-counter (OTC) options. The latter may be difficult to access for the common investor since OTC options are typically issued by large institutions without a central counterparty, limiting participants to accredited and institutional investors. Exchange-listed options are listed on public exchanges, encompassing a broader scope of retail and institutional investors with higher expected liquidity and potential insights into investor and market maker positioning.

In the equity exchange traded options markets, investors can find unique strategies to offset risk, generate income, or enhance portfolio performance. These strategies can be attractive diversification tools, and with recent uncertainty in the macroeconomic environment and the markets, the ability to attain optionality is in vogue. Option contract volume has doubled since 2019 as market catalysts brought new participants into the options ecosystem from self-directed investors to those who access the options markets via an ETF.1

Growing investor demand for optionality calls attention to how these markets function, including the role that market makers play, particularly with respect to the ETF structure. The liquidity that these large institutions provide gives investors access to public derivatives markets and confidence to trade in and out of exchange traded options. As a neutral party, market makers take a different stance to price moves in an option contract’s underlying assets while managing specific risks during the hedging processes. In this piece, we explain why it’s important to understand these dynamics from the market maker’s vantage point and the underlying plumbing in the exchange listed options market.

Key Takeaways

- COVID-19 was a catalyst for investors to use options as a way to limit risk and generate income. Fast forward to 2023, options usage continues to increase at a swift pace, putting the onus on market makers to maintain order and efficiency in these public markets.

- Market makers must mitigate risks unique to options to isolate their profit stream from trading activities while maintaining market neutrality. The five Greeks: delta, gamma, vega, theta, and rho, are risk measurements used by market makers to maintain order within their books.

- One of the key metrics that they use to manage risk is option delta, which measures linear risks embedded within an option. We elaborate as to how a market maker would use delta in practice to determine potential hedging trades.

Demand for Optionality Highlights the Role of Liquidity Providers

When the federal funds rates rapidly lowered to 0.25% in March 2020, income generation took on added significance for many investors, as did risk management capabilities of investment vehicles.2

As a result, equity options trading volume grew 58% year-over-year (YoY) in 2020, the largest such increase in equity options trading volume since 1976.3 Within equity options, one area of explosive growth as the pandemic unfolded was the index options markets.

From July 31, 2020 to July 31, 2023, daily open interest for index options on the S&P 500 (SPX) averaged $6.3 trillion, a substantial increase from $4.8 trillion from the prior three years.4 Daily open interest for the Nasdaq 100 (NDX) totaled $192 billion over the same period, up from $93 billion.5 Trading volume and open interest remained at record highs through the end of 2022.

With the appeal of options as hedging, capital efficiency, and potential income-generating securities continuing to increase, so too does the importance of market makers in this process. The efficiencies that market makers provide through their three main roles are what give investors an ease of access to the exchange-traded options markets.

- Provide Liquidity: Be willing to buy and sell securities at all times to ensure that investors can get in and out of the market quickly and easily at a fair price.

- Maintain Order & Efficiency: Quote two-sided prices (bid and ask) to help prevent large price swings.

- Promote Transparency: Disclose quote and trades to the public to allow investors to see what prices are available to make informed trading decisions.

Underlying these responsibilities is risk management, and how market makers manage their options risks is what makes these markets go. The goal of such risk management is to mitigate any form of markets specific risks in an efficient and timely manner.

Market Participants Monitor The Five Major Greeks With Different Goals In Mind

Owning or writing options creates unique risks. For example, equity exchange traded option contracts have a multiplier, typically representing 100 shares of the underlying asset, offering non-linear payoff potential. An investor can spend less money buying one option contract than purchasing 100 shares of its underlying equity asset outright, which creates economic leverage. Options market makers must account for this dynamic when they enact offsetting trades by monitoring options risks, known as the Greeks, to ensure that their profits and losses are isolated to their firm’s liquidity providing services. These services seek to minimize implicit trading costs for investors in the form of a bid-ask spread.

The five option Greeks are sensitivity factors that options traders, portfolio managers, and speculators use to manage their options portfolios and increase their profit potential. Each factor intends to measure how an investor can expect an option’s value to move in tandem with specified inputs based on contract specifications, government bond yields, or the price movements of the asset underpinning the contract to seek market opportunities. However, options market makers use the aforementioned inputs, represented by the Greeks, to react to risks already present in their options books.

Market Markers Must Offset Directional Risks

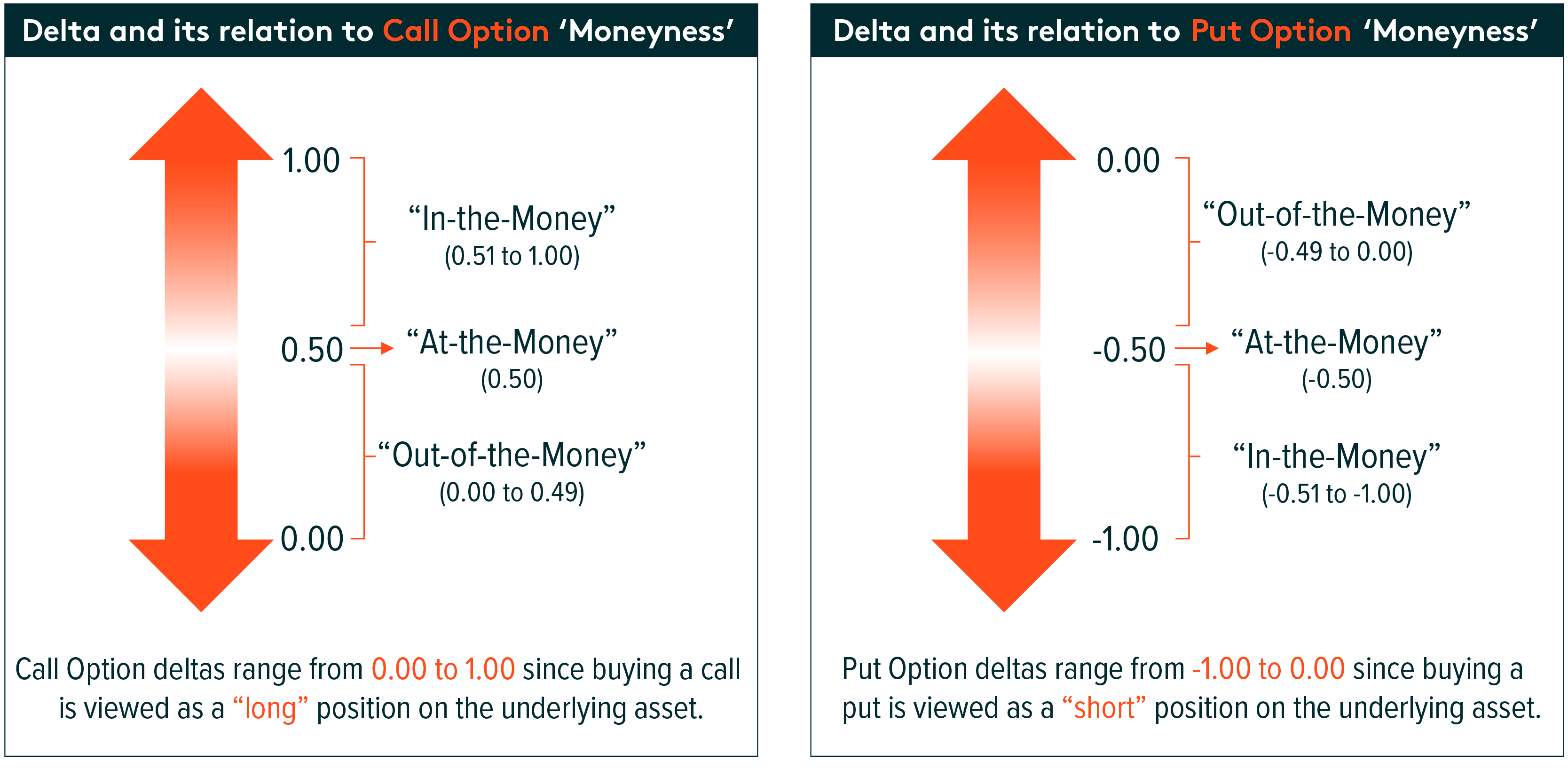

A highly monitored Greek and arguably the most popular, delta measures the change in price of an options contract for a $1 change in the price of its underlying asset. It is a linear measurement of an option’s price movement. For example, if a call option has an option delta of 0.60, it can be assumed that the call option contract will increase in price by $0.60 for every $1 movement in its underlying asset. As an underlying asset increases (decreases), a call option’s delta increases (decreases) until it reaches 1 (0). The opposite is true for put option delta movements. Once a call option’s (put option’s) delta is 1 (-1), it’s expected to move in tandem (inversely) with the underlying asset’s price movements.

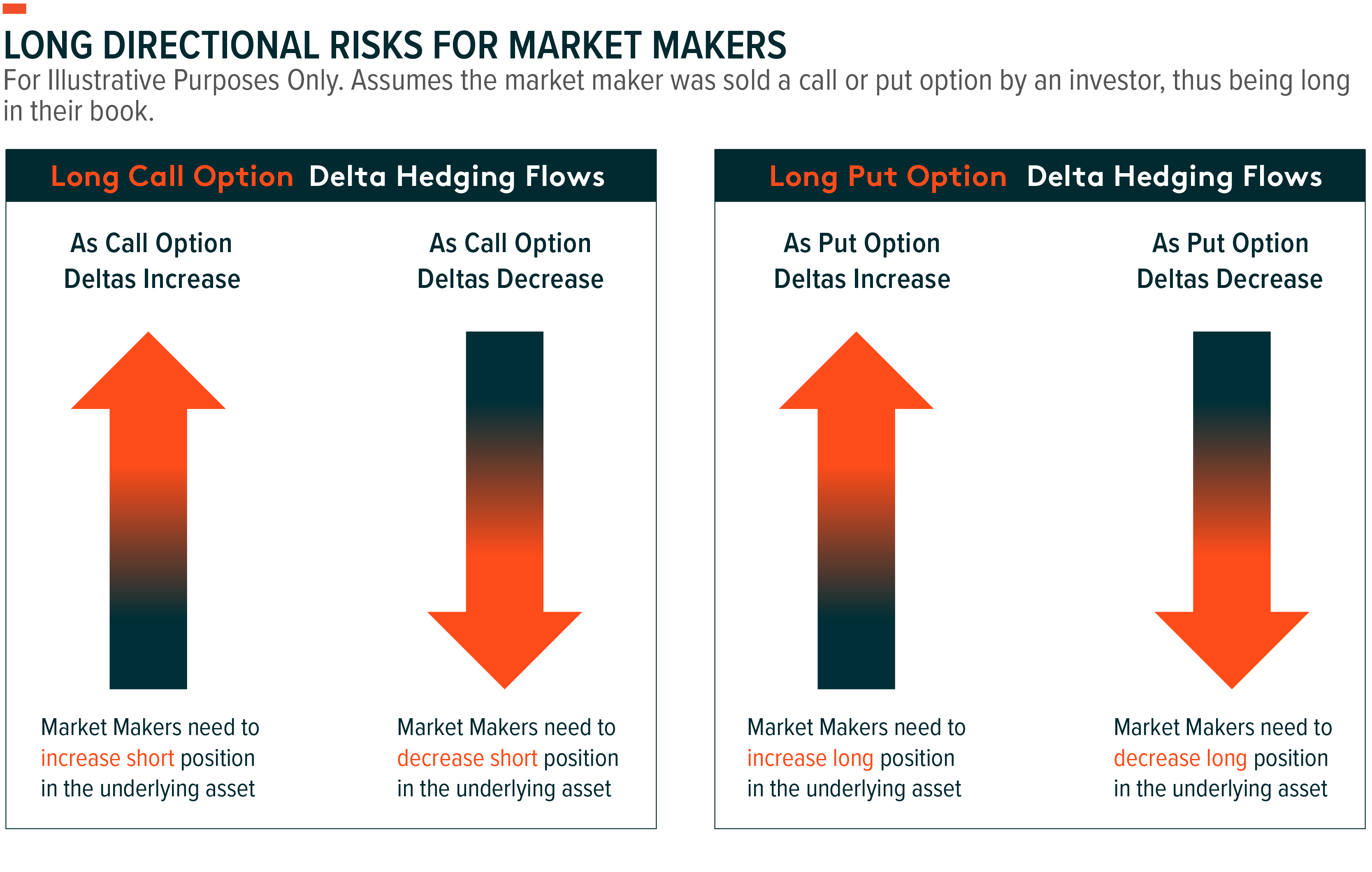

Due to the linear nature of delta, hedging against this sensitivity factor can be calculated in a linear fashion. For example, if a market maker added a long S&P 500 Index (SPX) call option position to their portfolio, it means that an investor initiated a short sell trade on this same SPX call option. In this hedging scenario, a market maker must hedge the long SPX call option exposure by shorting the same index to offset delta risk. Market makers have several ways to hedge it, such as shorting an SPX futures contract or an ETF tracking this same index. The opposite is true in instances where a market maker is hedging against a long put option position. To hedge against potentially, sharp movements in the underlying asset of an option, liquidity providers may implement different hedging techniques. One of these is gamma, which effectively measures how quickly delta moves, and is often referred to as the second order effect of delta. This is another particularly important consideration for market makers in their hedging process. This topic will be discussed more in depth in the next part of the series. We can see below how delta hedging occurs for both call and put option contracts from the angle of the market maker.

Conclusion: Options Market Makers Play A Unique Role In the Listed Options Markets

Optionality can bring diversification attributes to a portfolio, and investor appetite for these attributes has velocity of trading and open interest in equity exchange traded options trending much higher. Market maker management of associated risks to ensure that trading profits are isolated with minimal impact on the prices of the securities underpinning these contracts is critical to this market’s functionality. For investors, understanding how these players keep the inner workings of the exchange-traded options market in sync offers perspective on how and why they can access these markets.