Nearshoring and the New Countries Driving Growth in Emerging Markets

Globalization took off in the mid-1970’s with companies moving their supply chains to parts of the world that offered benefits such as cheaper labor and verticalization of supply. However, recent events, including the growing trade war between the US and China and the COVID-19 supply-chain crisis, have forced companies to re-evaluate their supply chains. In turn, companies have begun to look for other markets that are closer to their geographic homes but still offer benefits in terms of cost savings, in addition to both speed and security of supply.

Key Takeaways

- Nearshoring is gaining speed and relevance as “de-globalization” continues to take place, accelerated by growing tensions between the US and China and the COVID-19 supply-chain crisis.

- As China’s export dominance wanes, a massive opportunity is opening for other emerging market countries to fill the void, including Mexico, India, and Southeast Asian nations.

- The nearshoring trend appears to still be in its early innings, and we expect this theme to not only be relevant over the next two to four years, but for the next decade, as moving supply chains takes time to impact capital flows.

Catalysts for the Transition

Nearshoring is gaining speed and relevance as “de-globalization” continues to take place. Although China has gained share in US imports since entering the World Trade Organization in 2001, things have changed materially since 2018 on the back of the US-China economic conflict, which accelerated under the Trump Administration.1 As competition between the US and China increased, companies began looking at not just cost savings, but also supply-chain security through geopolitical uncertainty. The CHIPS Act and Inflation Reduction Act (IRA) in the US, in particular, focus on tech security within the supply chain. Currently, 70% or more of the world’s foundry capacity is in China and Taiwan.2 The US and EU are rolling out incentives to support a reshoring of semiconductor production. Taiwan Semiconductor Manufacturing Company (TSMC), for example, is already investing USD40bn in a new manufacturing facility within the US and is considering expanding in Japan and Germany.3 Strict and abrupt COVID-19 shutdowns, along with other growing costs in China, have also played a role in corporate decision making. For example, companies face higher intercontinental maritime freight costs, which climbed 545% from January 2019 to their peak in March 2022.4 Moreover, the carbon footprint for goods made in China can be much higher than in other nations, due to shipping, China’s reliance on coal power, and other factors. This is especially relevant in a time of growing ESG concern. Currently, world trade volumes are approximately 9% above pre-pandemic levels, however, the world is rapidly moving towards two major trading blocs, with one aligned towards the US and the other towards China.5 This is expected to bring both economic and geopolitical consequences, with trade between the two blocks likely to continue declining. Furthermore, the Russia-Ukraine war has accelerated many of these trends.

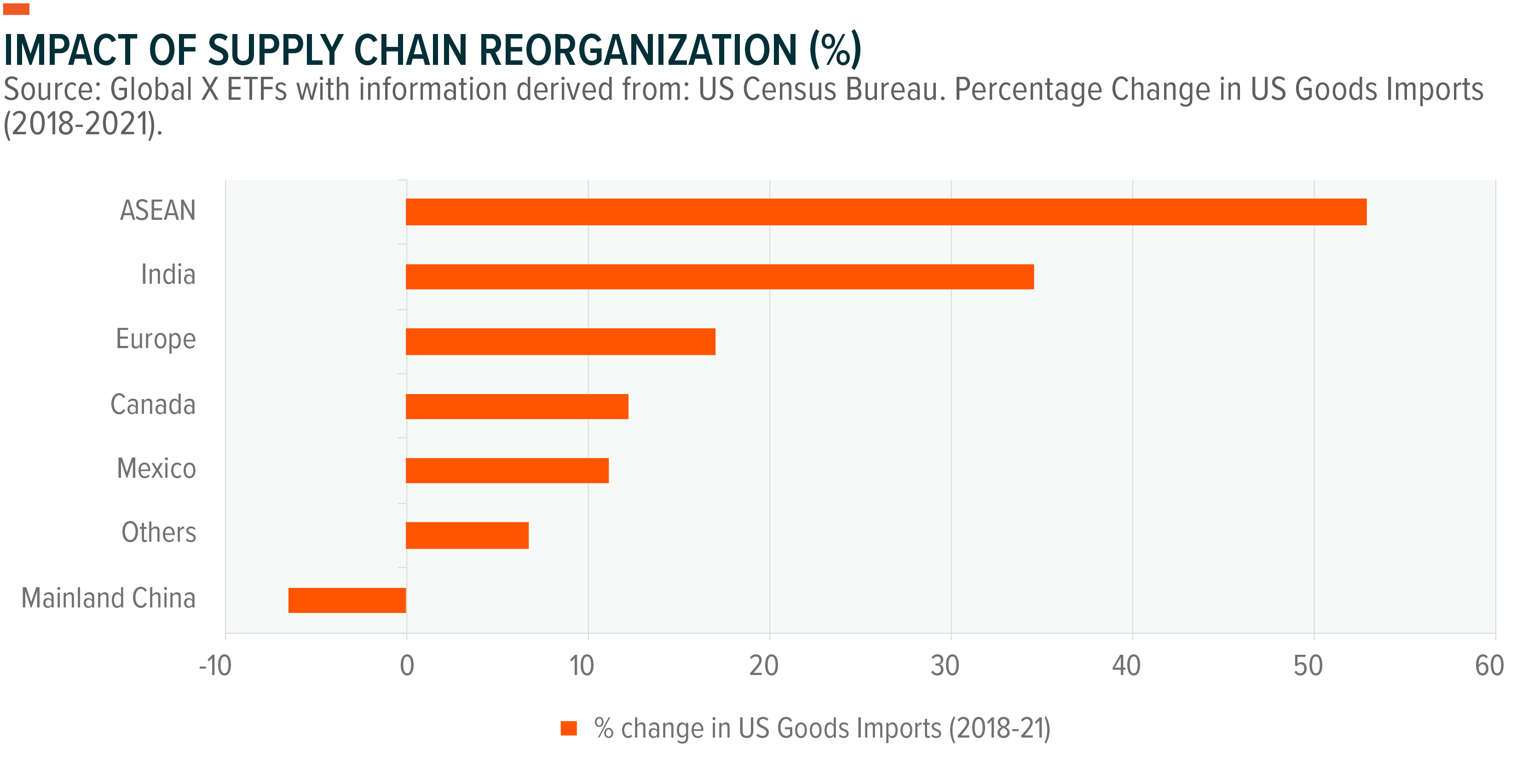

The chart below shows several “winners” from the shift away from Chinese manufacturing, including ASEAN countries (Association of Southeast Asian Nations), India, and Mexico. ASEAN countries were the first to benefit from “friendshoring.” Companies began gravitating toward countries that are near their existing operations in China, but have closer shared values, positive demographic trends, favorable policy reforms, and increasing trade cooperation. With US imports of goods reaching USD3,277.3bn in 2022, a 5% market share loss in China would represent roughly USD165bn in additional trade for other countries.6

Mexico

Mexico has been another key beneficiary of nearshoring. The country boasts an already large manufacturing sector; a strategic location as a US neighbor with significantly shorter transport times versus China; a high skilled yet lower-cost workforce; and good international trade cooperation on the back of the recently renegotiated North American Free Trade Agreement (NAFTA), aka the United States-Mexico-Canada Agreement (USMCA). Existing manufacturing ecosystems are already well integrated into the US, and new corporate policy agendas will probably drive future capital expenditure tailwinds. CBRE data show demand for industrial space in Mexico has doubled from 2020-21 and was forecast to double again from 2021-22, with approximately one out of every four square feet going towards nearshoring, about 70% concentrated around Northern Mexico.7 The recent decision from Tesla to build a battery manufacturing facility in Northern Mexico is evidence of both corporate interest in nearshoring and high demand for industrial space in Mexico. Our recent visit to Mexico coincided with Tesla’s final investment decision, which made the cover of several local newspapers and came up in all 24 meetings we had during our trip.

Mexico has typically been thought of as a high beta, or more volatile, play on the US economy, meaning that it is viewed as moving with greater momentum, either up or down, relative to the US. However, even with a slowdown in the US, remittances should continue to support domestic consumption and the peso, while ongoing nearshoring investments could offset a broader global slowdown. Current manufacturing exports from Mexico represented about 35-40% of that nation’s GDP in 2022 and should continue to grow as existing and emerging manufacturing clusters take market share from Asian economies, and thus potentially reverse trends since China’s entry into the WTO in 2001.8,9 The US imports some USD575bn per year from China compared to about USD450bn from Mexico.10,11 For each market-share point gain in US imports, Mexico’s GDP could increase by approximately 2.6%, or some USD33bn.12 In general, Mexico offers more geopolitical stability than China, as well as more robust intellectual property rights and environmental regulations. Moreover, wages, commodity costs, healthcare costs, and taxes tend to be lower than in China, on top of greater proximity to US end consumers. Despite the positive dynamics, Mexico probably still needs to improve its infrastructure, increase energy production, and continue growing its skilled labor in order to meet expected demand from nearshoring “waves” in the future. Unfortunately, the current AMLO Administration has been slow to act, and we view it as one of the main impediments to Mexico benefitting even more from nearshoring. In our view, Mexico needs to materially increase investment/GDP to build the capital stock needed to allow for more nearshoring expansion, and the government is slowly realizing this ahead of the 2024 Presidential elections.

India

India is quickly becoming the “China + 1” location, as supply chains move West, out of China. The country also benefits from a cost advantage with positive demographic tailwinds. However, India is also experiencing growth in manufacturing clusters on the back of a production-linked scheme that offers revenue-linked subsidies. Apple is another growth driver behind moving tech supply chains. The company helped China’s growth, given its involvement, local entrepreneurial drive, and government support. Especially given Apple’s size, it is a key player that can set standards and influence policy decisions. We see a similar trend now occurring in India, as Apple diversifies its supply chain into India and a burgeoning local tech-manufacturing ecosystem develops. Incumbent Chinese and Taiwanese companies will likely be the initial drivers but could eventually be replaced by local players.

Conclusion: We Expect Nearshoring for the Long Term

In general, companies with production that is spread across the globe could benefit from the regionalization of supply, as new factories in different geographies drive additional investment. Clients are beginning to prioritize flexible suppliers, which are generally multinational companies that have production hubs spread in different geographies but have commercial and management teams that are available in each market. We believe the nearshoring trend is still in its early innings, and we expect this theme to not only be relevant over the next two to four years, but for the next decade, as moving supply chains takes time to impact capital flows. Furthermore, nearshoring will likely benefit new sectors over time, such as healthcare, green energy, hardware, and batteries. Over time, as production bases are established, this should help raise local incomes, which could have spillover effects on the economies not just for lending, but also domestic consumption and tourism.