Why Passive Isn’t Really Passive

Editor’s note: The following post was initially published in 2017, but we feel has continued relevance to investors, in light of the evolving debate around active and passive management. The data was updated to the current period.

Not to get too philosophical, but twenty-plus years in the industry have taught me several truths. The first is that twenty years goes by quickly. The second, doing nothing is actually not nothing when investing. Technically, you’ve still actively decided to do something by holding back.

All Decisions Are Actions

You’re probably all too familiar with the debate about active versus passive management. In my view, it’s a waste of time. Now, that’s not because investors should overlook the merits of one or the other when building their investment strategy. It’s because the discussion largely misses the point.

There is nothing passive about investing. Nothing.

For one, the decision to invest is an act in and of itself. And that act alone triggers a series of events, requiring investors to get involved, even when utilizing index-based vehicles. It’s flatly incorrect to suggest that allocating capital toward a passive investment vehicle, such as an exchange-traded fund (ETF), is devoid of meaningful investor participation. It’s also incorrect to assume that it will run effectively, and in perpetuity, on autopilot. Because it won’t.

More Nuanced Than Appreciated

Building a properly constructed portfolio, one where asset allocation and diversification represent an investor’s risk tolerance and time horizon, takes work. As a first step, choosing the right building block—ETFs in our case—starts with understanding what ETFs are, and what they are not.

ETFs are not a singular asset class. They’re investment structures, formed by a portfolio of assets that will likely change over time, regardless of the strategy that governs these assets. That strategy could be to track the S&P 500 index or a low volatility version of the S&P 500. It could also be to track an S&P 500 sector or an MSCI international sector index. Potentially complicating the selection process is that indexes are based on sets of rules that are not entirely static, given the idiosyncrasies involved with rebalancing, additions, deletions, corporate actions, and general market dynamics. (ETFs can also be actively managed, pursuing a range of investment objectives without tracking an index.)

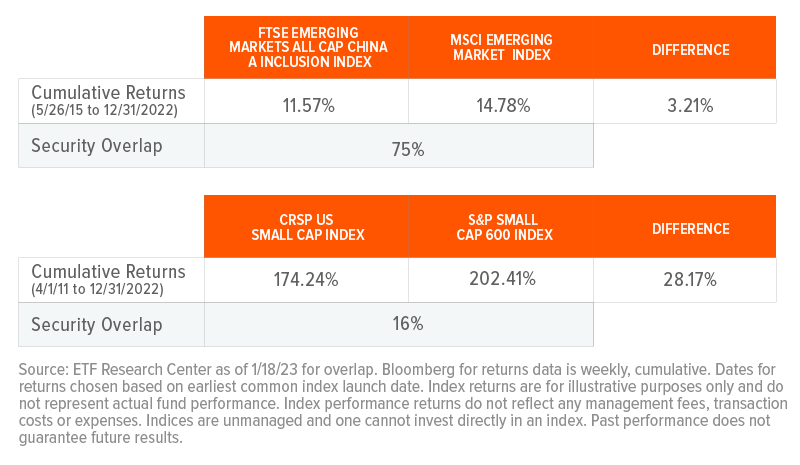

Major differences in returns and exposures in popular emerging market and small cap indexes:

Next, the manager needs to determine the right mix of stocks, bonds, currencies, commodities, or any number of alternative investments, such as private equity or real estate, to match or track the selected index.

And there’s more. Investors may need to consider that index strategies can employ a variety of weighting schemes for equities or fixed income. Weighting schemes include style boxes, volatility, factor tilts, and dividends in an attempt to achieve a better risk-reward balance than standard market-cap weighted indices.

Does all that sound particularly passive? According to Richard Bernstein Advisors (RBA), it sounds more like Pactive®, or RBA’s term for the active management of passive investments. Put another way, even when using a market cap-weighted index fund, managers must make decisions throughout the life of portfolios.

Watching the Portfolio Management Clock

Two additional decisions loom over the lifespan of an investment, arguably the biggest of them all. At some point, investors will likely have to decide when to change an allocation weighting or exit the investment altogether.

The passive strategy’s buy-and-hold tendencies do not mean, “buy and ignore.” Passive proponents, and historical performance, may argue that passive investments typically outperform active management. But investors still need to know how and when to pull the trigger on an investment. The clock with a passive investment ticks differently than that of an active endeavor, more focused on the big hand than the little hand. But the decision to close the investment is no less important.

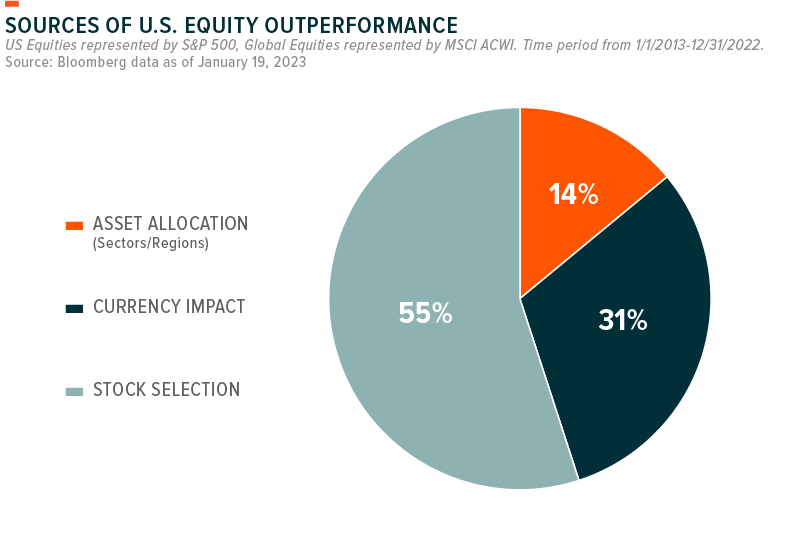

Take for example a simple decision of whether to allocate to US equities or global equities in mid-2009. In the 8-year period from July 2009 to July 2017, US equities outperformed global equities by a cumulative 78%.1 Yet, while stock selection made up over half the outperformance, 40% of the outperformance came from asset allocation and currency effects. Investing in passive products still means you’re making important market bets even when you’re not stock-picking.

A Certain Conceit

There may be a bit of stubborn pride at stake in the ongoing active versus passive debate. ETFs have increased in popularity, likely aided by their transparency, liquidity, and tax efficiency. Conversely, active managers, who are typically more expensive than an index fund, may be defensive about not outperforming their benchmarks in recent years.2

In my view, that underperformance can be attributed to a numbers game. Active management has historically underperformed when returns are concentrated in a few stocks. Unless those managers are willing to take on more risk, finding 100 basis points of excess return in an increasingly competitive environment can be challenging. Some may point to closet indexing as an alternative, but that’s likely a futile exercise. Active managers need to be truly active (high active share/concentrated) to deliver alpha versus the market.

Now, most acknowledge that stock picking can be difficult, especially when smart money is fighting smart money. But none of this active/passive stuff matters if the beta call isn’t right. ETFs are typically used to access less expensive returns, but it’s a misnomer to say that buying an ETF doesn’t preclude investors from the issues facing active management, namely what to buy, how much, and when. It all takes work

The takeaway? Passive investors still need to act as their own portfolio manager, including when investing in beta products, because they’re still making important market bets even when they’re not stock picking.